Buying Equipment: Accounting for Down Payments, Financing, and Ongoing Considerations

As a small business owner, I’ve learned that purchasing equipment is often a necessary step for growth. However, the accounting behind these transactions can be a bit tricky, especially when down payments and financing are involved.

In this post, I’ll break down the accounting treatment for buying equipment with down payments and financing, using my recent experience of purchasing a new industrial oven for my bakery as an example. We’ll cover both the initial purchase and the ongoing accounting considerations.

The Scenario

Let’s say I’m buying a new industrial oven for $50,000. I’ll make a down payment of $10,000 and finance the remaining $40,000 over five years at an annual interest rate of 5%.

Initial Accounting: The Purchase

Accounting for the Down Payment

When you make a down payment, you’re partially paying for the equipment upfront. Here’s how to record this transaction:

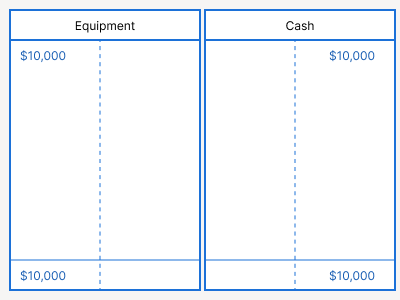

Debit: Equipment $10,000

Credit: Cash $10,000

This entry shows that you’ve increased your assets (Equipment) and decreased another asset (Cash) by the amount of the down payment.

Accounting for the Financed Amount

For the financed portion, you’re essentially taking on a liability (a loan) to acquire an asset. Here’s how to record this:

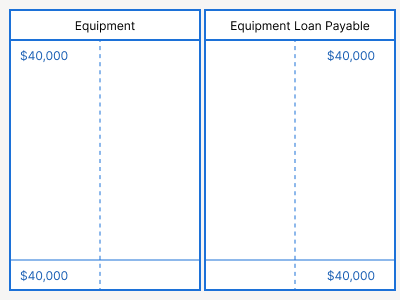

Debit: Equipment $40,000

Credit: Equipment Loan Payable $40,000

This entry increases your assets (Equipment) and increases your liabilities (Equipment Loan Payable) by the financed amount.

The Complete Picture

When we combine these two transactions, we get the full accounting picture of the equipment purchase:

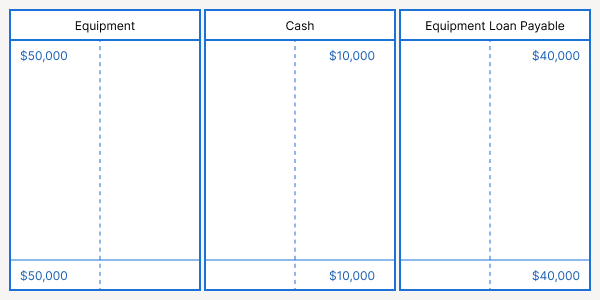

Debit: Equipment $50,000

Credit: Cash $10,000

Credit: Equipment Loan Payable $40,000This entry shows that you’ve acquired equipment worth $50,000, paid $10,000 in cash, and taken on a loan for the remaining $40,000.

Visual Representation

To help visualize these transactions, here’s a T-account diagram:

This diagram shows how the equipment account increases by the full purchase price, cash decreases by the down payment amount, and the loan payable account increases by the financed amount.

Ongoing Accounting Considerations

The initial purchase is just the beginning. Let’s dive deeper into the ongoing accounting considerations using our industrial oven example.

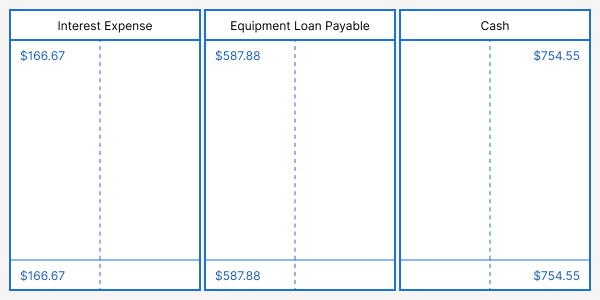

1. Recording Regular Loan Payments

We financed $40,000 of our $50,000 oven purchase at an annual interest rate of 5% for 5 years. Our monthly payment would be approximately $754.55.

Each payment consists of two parts: principal and interest. The interest portion is higher in the early payments and decreases over time, while the principal portion increases.

For example, in the first month:

- Interest: ($40,000 * 5%) / 12 = $166.67

- Principal: $754.55 – $166.67 = $587.88

The journal entry for this payment would be:

Debit: Interest Expense $166.67

Debit: Equipment Loan Payable $587.88

Credit: Cash $754.55

This entry reduces the loan balance, records the interest expense, and shows the cash outflow.

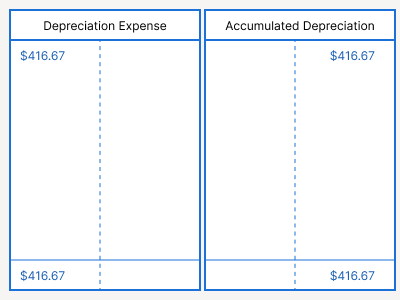

2. Calculating and Recording Depreciation

Depreciation spreads the cost of the equipment over its useful life. Let’s assume our oven has a useful life of 10 years with no salvage value, and we’re using the straight-line depreciation method.

Annual depreciation = Cost / Useful life

= $50,000 / 10 years

= $5,000 per year

Monthly depreciation = $5,000 / 12 = $416.67

The monthly journal entry would be:

Debit: Depreciation Expense $416.67

Credit: Accumulated Depreciation $416.67

This entry records the depreciation expense and increases the accumulated depreciation contra-asset account.

3. Tracking the Remaining Loan Balance

It’s crucial to keep track of the remaining loan balance for accurate financial reporting. After our first payment:

Beginning balance: $40,000

Principal payment: $587.88

Ending balance: $39,412.12

This process continues each month, with the interest portion decreasing and the principal portion increasing.

Putting It All Together: Monthly Accounting

Let’s summarize the monthly accounting entries for our industrial oven:

- Loan Payment:

Debit: Interest Expense $166.67

Debit: Equipment Loan Payable $587.88

Credit: Cash $754.55- Depreciation:

Debit: Depreciation Expense $416.67

Credit: Accumulated Depreciation $416.67Impact on Financial Statements

Balance Sheet

- Equipment (Fixed Asset) remains at $50,000

- Accumulated Depreciation increases by $416.67 each month

- Equipment Loan Payable (Liability) decreases by $587.88

- Cash decreases by $754.55

Income Statement:

- Interest Expense of $166.67 is recorded

- Depreciation Expense of $416.67 is recorded

Cash Flow Statement:

- Operating Activities: Interest paid ($166.67)

- Investing Activities: No impact after initial purchase

- Financing Activities: Principal repayment ($587.88)

Conclusion

Understanding the accounting treatment for equipment purchases involving down payments and financing is crucial for maintaining accurate financial records.

By breaking down the transaction into its components – the initial purchase, ongoing loan payments, and depreciation – you can ensure that your books correctly reflect your new asset, the reduction in cash, and the new liability you’ve taken on.

Remember that this accounting process continues throughout the life of the equipment and the duration of the loan.

By keeping accurate records of these ongoing transactions, you ensure that your financial statements reflect the true financial position of your business, the actual cost of using the equipment over time, and the remaining obligation on the loan.